Evergreen Financial Planning for Freelancers and Independent Contractors

fddd

With the market's projected economic slowdown in 2019, this year

might bring some challenges to freelancers and independent contractors who rely

on project-based work to pay the bills. Evergreen financial planning is critical.

Luckily, there are steps you can take to invest, protect and

plan for your financial health, regardless of economic conditions. By exploring

available options, you can select those that best fit your vision, values and

goals for investing your wealth. These tools and resources can get your money

working for you, in good economic times and bad.

There are many challenges that freelancers and independent

contractors face that W-2 employees may not. Projects may not pay consistently,

or work projects may slow to a trickle, leading to inconsistent cash flows.

Follow these strategies to build more wealth from what you bring home.

Strategy 1: Manage

liquidity

There are two primary ways to structure your portfolio to

generate cash when you need it.

- Passive.

Increase revenue streams by looking into investments that can generate cash for

you. During cash valleys, the dividends and interest generated by these

investments are a great additional source of income, without dipping into your

principle. When you are flush, the money you don't use day-to-day is simply

reinvested. - Active.

Invest in more liquid assets, such as publicly-traded stocks, bonds, real

estate investment trusts, and other assets that can easily be sold. If you buy

an individual stock such as Apple or a share in a mutual or exchange traded

fund today, you can sell it tomorrow. However, if you buy into a hedge fund or

non-public business, cashing out when you are in need may be problematic.

Read more: What

does it mean to own a moderately balanced portfolio?

Strategy 2: Fund

retirement

As a freelancer or independent contractor, your tax profile is

different from W-2 employees. You are required to pay quarterly taxes and have

different retirement savings vehicles available to you.

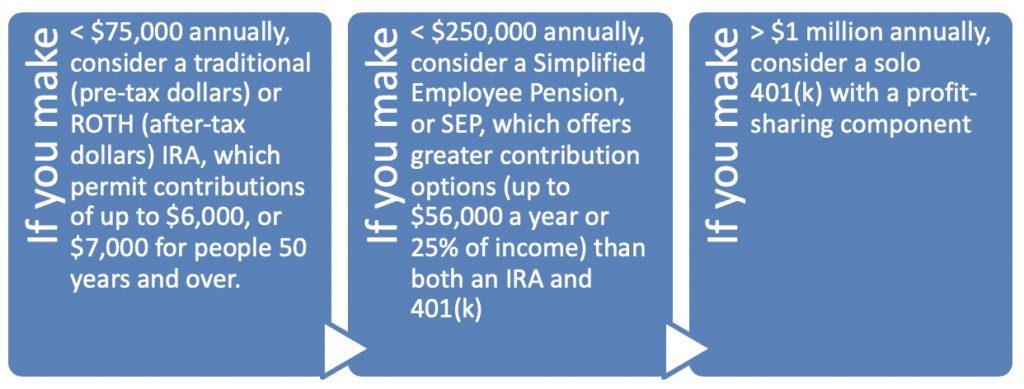

Selecting the right retirement vehicle depends on how much you want to save and your tax bracket. Let's break it down by income levels.

A freelancer making a maximum of $25,000 a year might prefer

to fund retirement with after-tax dollars in a ROTH IRA. A freelancer making

more, up to $75,000 a year, may choose to fund retirement with a traditional

IRA to take advantage of the tax deduction. Contributions are limited in both

IRAs to $6,000 for the under-50 crowd and $7,000 for individuals over the age

of 50.

For higher-income earners making up to $250,000 a year,

consider another alternative, a Simplified Employee Pension, or SEP. A SEP plan

offers greater contribution options than an IRA or individual 401(k).

High-earners might consider a 401(k) profit-sharing plan.

This plan lowers an individual's tax burden immediately and only needs to be in

place for three years to reap the greatest rewards.

The profit-sharing component allows you to tax-efficiently

take profits out each year, while the 401(k) component allows you to make

pre-tax contributions for retirement (up to $19,000 for taxpayers under the age

of 50 and $25,000 if 50 and over).

Read more: Stacking

retirement plans accelerates savings and reduces taxes

Strategy 3: Protect what

you own

Wealth needs to be protected. In the wealth management

arena, the term "asset protection" has different meanings and uses. Generally,

it shores up capital against threats from litigation, market turns, fraud and

more.

While there is no way to guarantee asset safety, there are

asset protection strategies that can help shield your assets from unauthorized

access. This might include insurance binders, trusts and offshore accounts, or

investment portfolio strategies, such as bulking up on bonds and non-correlated

asset classes to hedge against market risk. Talk to a wealth advisor about how

to best minimize risks to your assets.

Read more: Lawsuits,

Bears, and Bad Actors: Make Protecting What You Own a Priority

Strategy 4: Integrate

tax planning

Every financial decision has tax and legal considerations.

Minimize your tax bill by understanding what those consequences will be before

making key decisions. This is especially important for high-income earners that

have more to lose when taxes are ignored.

Work with an investment advisor that knows your tax

situation and works in tandem with a tax specialist so tax considerations are

comprehensively integrated into your financial plan.

Read more: Take

a bite out of your tax bill with tax-efficient solutions

Strategy 5: Point

your financial compass in the right direction

Personal finances are one of the most intimate and emotional

conversations we can have with others, which is why so many women find it

difficult to talk about their financial affairs. Learn how to talk money with a

network of like-minded family, friends, and trusted advisors. These outlets can

connect you to resources and solutions that support your financial health for a

lifetime. Join the Women, Wealth & Wisdom network to make connections and

get additional resources for achieving your long-term financial goals.

The earlier you get the conversation started, the healthier

your asset portfolio will be. Start 2019 on the right foot and get your

financial compass pointed in the right direction.

Watch now: Where's

your financial compass pointed?

About the Author

Cindy

Alvarez is a Senior Wealth Management Advisor at Wambolt & Associates in

Colorado, where she has been helping clients achieve their financial goals

since 2012. She is also the driving force behind Women,

Wealth & Wisdom, a women-only educational series and group mentoring

program for building and preserving wealth. Click here to

join with other women taking control of their financial future. Cindy can be

reached at cindy.alvarez@wamboltwealth.com or

720.962.6700. http://www.wamboltwealth.com

Our Blog Wars was a huge success! Please feel free to submit a blog anytime.